Online Advertising Companies

Personal Context: The recent drop in Facebook market cap (July 2018) was the trigger to this further analysis. Add to that, a recent twitter discussion on S&P 500 stocks pie chart made me wonder about the contributions of the top few stocks. My personal investing experience has primarily been in the early -mid stage growth private companies in the valuation range of $20 – $500 million. By contrast, the smallest company in S&P 500 has a market cap of $4 billion. And the largest are close to a trillion dollars. The idea of this post was to get a better understanding of some of the world’s biggest companies. In this post, I explore Facebook, Twitter and Alphabet, and the Online Advertising space.

The companies: How do you determine which are some of the world’s biggest companies? I looked up the Forbes Global 2000, Fortune 500 lists, the S&P 500. And then a general google search on private companies. The trigger for this post was Facebook. The space that Facebook operates in is led by Alphabet/Google. And Twitter is a small (comparatively) player in this space.

The analysis: A starting point for me is the value, or say, market cap. Next is to understand the revenue and its drivers. Revenue by itself means little, unless presented with a qualifier of income on that revenue and may be, the free cash flow. And to add a bit more depth, the growth rate, the trend and a colour on business drivers. Not a lot. But I think if we begin with these numbers and a sense of the market they address, it should help gain familiarity with the scale and context of these companies.

Data Source: Mainly the company annual reports. And then some online stock databases.

Additionally, since I started writing this, for my own benefit, I have added a context note on how big some of the biggest companies are. And where some of these large companies stand vis-a-vis the global market cap. Available here.

Advertising | One man’s expense is another’s income

Advertising is a necessary expense for many companies. The global advertising spend is around $540 billion in 2017(?). I couldn’t find consistent data, but the numbers are in the ballpark broadly. This number was $329 billion in Year 2000. The industry has since grown at 3% pa. These are advertisements across TV, print media, radio, outdoor, cinema and internet.

Internet was 2% of the spend in 2000. It has grown to 38% in 2017. It has grown the pie, and also taken some of the share off other channels. The way the world consumes media, and hence the preferred ad channels have changed considerably over this period.

Consider the following pie charts – Year 2000 spend, and Year 2017 spend.

It is just the way the world is now. So much more time is spent online. As one report somewhere mentioned that for the purposes of advertisers, US consumers now 31 hours instead of the usual 24 given the multitasking and attention distribution across different online & video channels. As to how this Internet Advertising is distributed across different categories, it is mainly Search, followed by Social.

The companies discussed here, (Google, Facebook, Twitter) operate in this new big market of Internet Advertising. Although the total ad spend has grown by 3% pa, the internet ads market has grown by over 20% yoy.

The interesting bit is if we just add the numbers, it seems that between the three companies (or actually, between FB and Google), they seem to control three-quarters of the global internet spend (!?)

And hence, the question of future growth. How far can the numbers go from here? TV ads continue to grow. Another big category which has held strongly to its share of the pie. Others have shrunk, but how far?

Let’s take a look from another angle to get a better grasp of these numbers. From the perspective of the spenders. It seems like 5 companies spend around 8-9% of the total ad spend. And here too, data has been difficult to corroborate. But the five companies according to AdAge are as follows: P&G, Unilever, Nestle, Samsung and L’Oreal.

From P&G’s annual report, I understand that the Ad expenses are $7.1 billion. (Media agencies/ AdAge estimate it to be $10 billion). I am unable to spot the exact item in other reports (Unilever, Nestle). L’Oreal spent around $8.8 billion on Ads and promotions in 2017 per its financial presentation. For the other three companies, agencies estimate it in the $9 billion range.

All five of these are sort of old-world companies, mature businesses. But there is another category – that of fast growing new-age spenders like Amazon and Alibaba. I plan to explore them soon given they fall in this blanket category of really big companies.

In another intriguing data point, some 100 top spenders (companies) spend around 50% of the total global ad spend. They must be spending across all channels, not just internet. However, if we then think of the customers for the companies like Facebook and Alphabet, and where the advertising dollars are coming in from, these 100 big spenders must be forming big accounts.

The companies | Facebook, Twitter & Alphabet

Alphabet and Facebook are the key players in the online advertising space. Following is a snapshot of these businesses for reference.

The Annual Revenue from Calendar year 2013 to year 2017 and for Trailing Twelve Months ending June 2018:

For the same period, the Net Income interestingly have moved like the following. All numbers in $ billion.

Before we get into the details on each, as a summary, here is the three of them – Facebook, Twitter and Google in a comparison. Given the market cap and TTM (Trailing Twelve Months ending June 2018) numbers, not sure how this post ages. But here at the moment, these businesses side by side look as follows:

An interesting feature of all these businesses is that they are mostly B2B business. They need users, and lots of them, and need to provide them a great experience, but their main customers are other businesses wanting to advertise on these platforms. In a way, although the services are ‘free’ for the users, the eventual build-up of costs and advertising spend for the ‘customers’ of these businesses will eventually be indirectly passed on to these very free users.

There’ll be a subset which are users as well as customers, and may be a growing subset, but still, a small portion of the overall business.

Here, following is a bit more detail on each of these companies.

Facebook was the trigger to this post; so I’ll begin there.

The standout fact: As I started looking at the numbers in detail, one of the facts that stays the highlight for me is its high Income from Operations (I’ll refer to it as OI). I have not been following these stocks, but an Operating Income of $20 billion (for 2017) is very impressive even as a stand-alone number. Compare it to Amazon’s $4 billion for 2017, although Amazon’s June 2018 TTM (Trailing Twelve Months) OI is close to $7.4 billion.

Very few companies can boast an Operating Income margin of 50% and Net Income of 40%. Especially companies as large as $48 billion reported in revenue.

Here is a snapshot of FB numbers for the last five years or so.

What is Facebook? The platforms of Facebook, Instagram, Messenger, Whatsapp and Oculus. Employs around 25k people. Founded in 2004, listed in 2012. Mark Zuckerberg controls the majority decision making in the company.

Now, what makes revenue for Facebook? Revenue is mainly ad income (98%) – Ads displayed on all its platforms. And a tiny portion is revenue from payments and other fees. Advertisers/ companies and people around the world pay FB around $48 billion annually for displaying ads on its platforms. The payments are linked often to clicks, and sometimes to impressions. Although FB converts everything to impressions basis.

The total Daily Active Users (DAUs) for FB were 1.47 billion on average for June 2018, and Monthly Average Users (MAUs) were 2.23 billion for that month.

2.23 billion monthly average users. World Population is 7.6 billion people. Or around 30% of the world accesses Facebook on a monthly basis (!?) and 20% or 1 in 5 people access it daily!

Hence the number of users has been one of the primary driving forces for Facebook’s revenue over the years. Since 2013, the revenue has grown at a CAGR of 51% and Net Income at 81%.

The brouhaha is partly driven by the fact that Facebook is not going to grow the way that it has grown in past. In five years, Facebook has grown more than five times of its 2013 revenue. Such growth for companies of mammoth size is really hard to come by.

![]()

I have added Twitter in this analysis for comparison. It is not a ‘large’ company but operates in the same space as Facebook. Twitter is also a platform for sharing. Their main source of revenue is advertising, which is generated through Promoted Tweets, Promoted Accounts and Promoted Trends.

Twitter was set up in 2007. Employing around 3.3k people. Compared to Facebook, Twitter is a much smaller company. It has around one-twentieth of FB’s revenue and market cap.

For a moment, one could wonder whether it is a time-lost cousin of FB? But after operating for around a similar time scale, they still seem to scrape through on NI basis. (Where FB has one of the best profitability numbers one comes across in long times).

Around 86% of Twitter’s revenue is from advertising. Rest comes from Data licensing and other revenue. US represents 58% of revenue sources. Although the revenue growth CAGR (from 2013- 2017) is around 38%, what is worth noting is that the growth seems to be stalled in the last 3 years.

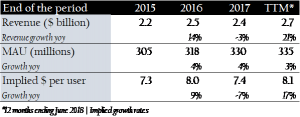

Twitter has around 335 million monthly active users. (Around 15% of Facebook MAUs). And I couldn’t find the DAUs for Twitter. So, running the numbers here on MAUs.

Alphabet

Now, a look at the key player in this space of online advertising. Or the leader.

What is Alphabet? Alphabet is the holding company (2015) for Google and its various businesses. Google was set up in 1998. Employs around 72k people. The key source of revenue is from its multiple platforms of Search, Ads, Commerce, Maps, Youtube, Google Cloud, Android, Chrome and Google Play. The main revenue is advertising revenue across its own and network properties.

Interestingly Google’s share of Ad revenues is also 86%, similar to Twitter, but the ad business is 45 times that of Twitter or 2.4 times that of Facebook.

As one can now see, Facebook’s OI is high. Compare it to Google, which has 2.8 times its revenue, but OI is only 1.4 times. Or where Facebook’s OI is close to 50%, Google is at 26% of revenue. US is 47% revenue. I am not delving deeper in Google at the moment which perhaps requires an independent post.

Concluding thoughts

When I started exploring these companies, I had a few different questions which I was seeking answers to. That of questioning the assumption of perpetual growth in valuing companies. And that of understanding what is the theoretical maximum that a company can reach?

Hence, the meandering path through the context setting and trying to get a sense of the market for these businesses.I still don’t have the answers but a few more questions yet to be explored.

When companies are so big, they seem to operate in a different universe. The rules that apply to average companies seem to stop applying to them. There is the point of immediate future (next few years), immediate past (last few years), and the longer term, where the perpetual growth comes in play. When one thinks that between them the two companies cover 75% of a market, they grow by creating more market and then by taking share from each other. So, two different growth rates: that of the category itself which they both help in increasing the pie, and then the question of individual growth, where they compete with each other. Finally, growth at what cost. Eventually, if the numbers do not filter through fast enough to the bottom line, the big question of perpetual growth on what level of cash flow?

As a personal view/ user view – for a company like Google which has lots other stuff in the play, and has a stickiness given search and platforms which seem to get non-discretionary in nature with time, there is more certainty of continuing to hold its place, even if there might be questions on how much it can grow from here. But for something like Facebook, although it has one of the best profitability ratios, still seems like a discretionary category of time spend.

Further questions

I think this post has spread out more than it has dug deeper. There are still layers and layers in each of the above explored items. Immediate questions/ things to look up

- One of the ways to further explore them is the R&D spend.

- Then again, the user and click data. And further granularity on the long-term nature of these revenues

- How is the business model going to evolve? So far, the driver has been consumer behavior change. More users, more time. Has it all settled in a long term pattern or more movement yet? If it has settled in a long term pattern, then is the valuation justified?

- Google’s net income in recent times – why so low?

- A deeper look at the Marketing P&L of few of the ‘customer’ companies.

- What are the other companies that share the rest of the market?

Closing Note: The objective of the note is to get a perspective on a few large companies. I have referred several web-links and data points for this note. The data referred is quite spread out, and I have tried to consider and compare several sources to arrive at the above. Still, the numbers may not be exact, but they are close enough or approximated to get the broad picture. Happy to be corrected if you spot any glaring errors of fact or thinking. And keen to hear more on the open questions.