Research & Development spends

I came across a chart today about R&D spends by different companies (the chart is from howmuch.net and is shared at the end of this post). That eventually led me to a data-set by PWC Consulting arm strategy&. They have been doing this analysis on R&D spend for a few years now. They have shared data on 1000 top R&D spenders (Dollar volume) from public companies’ universe along with their revenue details for the last seven years. Links at the end of the post.

I got pulled into the data, and spent some time browsing through the list, and looking up some of the companies. Following are some notes, thoughts and takeaways, mainly stuff that stands out for me.

The top 1000 companies spent $782 billion on R&D in 2018.

A note here that this is a broad and general number. I realise that when they mention 2018 revenue or R&D figures in the excel sheet, it could mean results published during the year until June 2018. For example, they do not have the FY18 number for Apple (year ending Sept 2018), but even the FY17 number for Apple is high enough to be in top 10. (And so goes for many other companies)

In the study methodology, they mention the following:

“1000 companies collectively account for 40 percent of the world’s R&D spending, from all sources, including corporate and government sources.”

Takeaway #1: What this means is that total global R&D spend is about $2 trillion.

Around 166 companies have spent over a billion each on R&D with a total of $544 billion. 11 companies have spent over $10 billion each with a total of $ 148 billion.

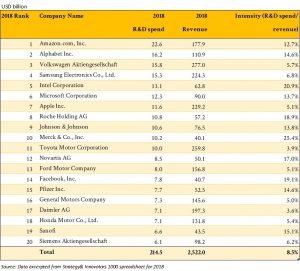

For reference, I have pulled out a list of top 20 R&D spending companies and their revenue, as well as a R&D intensity (R&D spend as a % of Revenue)

Spend or Investment?

R&D spend or Research & Development is one of the integral spends for any company (Other costs relate to production or procurement, advertising and marketing , selling, personnel and other administrative costs). Philosophically, R&D is the phase before production or procurement, and is an answer to the ongoing existential puzzle around the future of company. The spend has little immediate revenue to show, but it is the promise of the future. The spend could be necessary to incur just to stay in place (where the sector is on treadmill and the spend is necessary to maintain the spot), or it could be leap-forward spend (for future market creation and capture).

R&D spend include both research as well as new development costs. The idea is eventually, market or products will be created which will create revenue for the company. Directly or indirectly, the spend flows and manifests itself into intellectual property, the brand, new products, new needs, new markets. Also, there are normally credits or tax incentives provided by governments around the world for R&D spend.

There are accounting standards for treatment of this spend basis on the nature. At times, companies prefer capitalizing expenses so that it does not affect annual profitability, but capitalization is not easy simply because the estimate of revenue which can be directly attributed to the is not easy. The methodology mentions the following:

“Starting in 2013, we included the most recent fiscal year’s amortization of capitalized R&D expenditures for relevant companies in calculating the total R&D investment, while continuing to exclude any non-amortized capitalized costs.”

The components of the R&D costs can be people costs, materials, infrastructure and external projects.

As to specific reasons for companies incurring the spend, as examples, consider the following excerpts from a few annual reports, where companies explain their investment or spend for R&D.

Apple incurred R&D spend of $14.2 billion or 5% of its revenue in FY18 (September YE). Compare this cost to their Selling, General and Administrative cost of $16.7 billion. So almost half of Apple’s operating costs are R&D costs. Apple’s FY18 operating income was $70 billion. Apple is one of the most profitable companies in the world.Not many companies in the world have that high a number of operating income ($ volume). And Apple operates in a relatively saturated market. They spend to create tomorrow’s markets for its products. Following is from their Annual Report:

“Because the industries in which the Company competes are characterized by rapid technological advances, the Company’s ability to compete successfully depends heavily upon its ability to ensure a continual and timely flow of competitive products, services and technologies to the marketplace. The Company continues to develop new technologies to enhance existing products and services, and to expand the range of its offerings through R&D, licensing of intellectual property and acquisition of third-party businesses and technology.”

Volkswagen group. They incurred $15.7 billion or 5.7% of their revenue. (According to their annual report, it is 6.7% since they count what they capitalize as well). They are the third largest global spender on R&D, the highest in any other sector apart from tech or pharma. The spend levels are similar to that of Apple (in dollar terms) but compared to Apple, which as a ratio, spends around a fifth of the operating income on R&D, they spend an amount equivalent of their operating income on R&D (which I find intriguing! Must be a discussion point with their investors. To look up). They spend on stuff like research of lightweight materials, renewable fuel, carbon-neutral combustion engines etc. Following is an excerpt from their most recent annual report:

“Research and development costs comprise a range of expenses, from futurology through to the development of marketable products. Particular emphasis is placed on the environmentally friendly orientation of our product portfolio. The R&D ratio underscores the efforts made to ensure the Company’s future viability: the goal of competitive profitability geared to sustainable growth.”

“As of December 31, 2017, our Research and Development departments – including the equity-accounted Chinese joint ventures – employed 49,316 people (+2.6%) Group-wide or 7.7% of the total headcount”

Johnson & Johnson. J&J spent $10.5 billion on R&D or 13.8% of revenue. A high portion of the operating income. (Not as high as VW above, but significant given the intensity of 13.8% of revenue). The spend is grouped in three categories of consumer, pharma and medical devices with major portion going in pharma. Following is from their annual report:

“Research activities represent a significant part of the Company’s businesses. Research and development expenditures relate to the processes of discovering, testing and developing new products, upfront payments and milestones, improving existing products, as well as demonstrating product efficacy and regulatory compliance prior to launch. The Company remains committed to investing in research and development with the aim of delivering high quality and innovative products. Worldwide costs of research and development activities amounted to $10.6 billion, $9.1 billion and $9.0 billion for fiscal years 2017, 2016 and 2015, respectively. Research facilities are located in the United States, Belgium, Brazil, Canada, China, France, Germany, Israel, Japan, the Netherlands, Switzerland and the United Kingdom with additional R&D support in over 30 other countries.”

Facebook. For an indication of why some of these R&D expenses can be so high, it can be high people cost. Take the following from Facebook’s annual report. Facebook is another company which I believe is very profitable for its size, and although it spends 19% of its revenue on R&D ($7.8 billion), since its operating income is high, at ~50% of revenue, the portion of R&D from profits is lower than say VW or J&J above.

“Research and development. Research and development expenses consist primarily of share-based compensation, salaries, and benefits for employees on our engineering and technical teams who are responsible for building new products as well as improving existing products. We expense all of our research and development costs as they are incurred.”

Worth noting here that R&D can be quite subjective. And may not be comparable across companies. Hence, the whole analysis needs to be considered as a broad-brush/ indicative analysis.

Different sectors have different R&D intensity

R&D spend can be a more important and bigger bucket in certain sectors than others. Consider the following table of industry groups of the top 1000 spenders grouped (2018 R&D spends per the excel sheet). Understandably, the highest spend is in the tech (software, hardware) or pharma (+biotech and related) sectors. Both sectors where a lot of new developments happen and obsolescence is high.

Tech accounts for $204 billion, or 26% of the total spend of top 1000. Pharma, Biotech, Life sciences and healthcare equipment accounts for $174 billion or 22% of total.

Takeaway #2. Automobiles are high up along with Tech and Pharma. (I had thought it would be other players like Defense. But not much on defense. There are 33 companies classified as Aerospace or Defense amongst the top 1000 incurring a total spend of $22 billion.) I understand that the sector needs continuous investment in new developments, esp with all players looking at fuel efficiency or electric vehicles, and related problems of energy storage etc, but still, the spend levels seem high. Automobile sector with spend of $ 120 billion on R&D accounts for 15% of the top 1000.

All together, tech, pharma and automobiles account for 63.7%. Further, there’ll be other categories that can be grouped in the bigger blanket of tech such as semiconductors. If you add semiconductors, the tech bucket accounts for a third of total top 1000.

Another way to look at these sectors is as a portion of revenue. Before looking at individual companies, a quick look at the sectors and intensity on grouped revenue. The sectors where intensity is above average, are in bold.

What are the implications here? Companies operating in or entering any of these high spend sectors have to layout a big portion of budget and investments for R&D. Another point worth noting from above: interestingly, per above table, the R&D intensity in automobiles is not that high. It just says 4.1% , much lower than the other top 2 sectors. So, Volkswagen is not much far out, just above average spend in the sector. In one of their investor presentations, they mention approaching R&D costs with a critical look.

If one were to look at the top companies, amongst the top 20, a few standout companies for me are the following:

Amazon with a revenue which is not very profitable, spends $22.62 billion on R&D, or what they call Technology & Content costs. They are the list toppers. As a % of revenue, it is just 12.7% but then their revenue is a low GM revenue. They spend to evolve into something that can create more profitable set of revenues in the future (such as better Alexa or AWS). What is interesting is that this number is over five times Amazon’s OI number. After looking at their treatment and comparing it to others, a takeaway is that not all R&D is comparable. Especially, that of Amazon. It is a unique company, mainly because of its size, and secondly because its main business does not make money, but is sort of a loss leader for the new evolving business lines. They cannot be easily bucketed into any category. They are so big, that they change the dynamics of the market around them. Following from their annual report:

“Technology and content costs include payroll and related expenses for employees involved in the research and development of new and existing products and services, development, design, and maintenance of our websites, curation and display of products and services made available on our websites, and infrastructure costs. Infrastructure costs include servers, networking equipment, and data center related depreciation, rent, utilities, and other expenses necessary to support AWS, as well as these and other efforts. Collectively, these costs reflect the investments we make in order to offer a wide variety of products and services to our customers.”

Intel with over 20.9% of revenue in R&D. Following from Intel’s annual report.

“We are committed to investing in R&D. Realizing the benefits from Moore’s Law provides flexibility in balancing production costs and the increased functionality of our products. In addition, intellectual property that we have developed for our platforms reduces our costs, creates synergies across our businesses, and provides a higher return as we expand into new markets.We design and manufacture silicon technology products. Unlike many other semiconductor companies, we primarily manufacture our products in our own manufacturing facilities. We see our in-house manufacturing as one of our most critical assets and advantages. This advantage is now expanding to our adjacent businesses, for example, FPGA, modem, and memory, which are enabling our transformation to a data-centric company.”

Then there are these high intensity companies – all the pharma/healthcare companies like Roche (intensity of 18.9%), Novartis (17%), Merck (25.4%), Calgene Corporation (45.4%), Astrazeneca (24%), Eli Lily ( 23%).

As I look at the data from top intensity (highest R&D spend on revenue), I arrive at my next takeaway. There is a bit of random data (companies with negligible revenue), but as you sift through it, you come across a series of companies in the Healthcare/pharma/biotech sector. So for me, the intriguing Takeaway #3 is that there seems to be a lot of early stage/ little revenue making pharma/ biotech companies are public. Revenue promised perhaps but not yet delivered. What is interesting or worth further exploring is that why is it so that in tech sector, such companies will still be in private hands, while in biotech they are already listed. Is it because that the conversion of R&D to revenue is much longer holding in Biotech than revenue and once converted, obsolescence is relatively lower?

Take for example, a company picked at random from the list. Coherus Biosciences (Number 711 on the list, spent $254 million on R&D in 2017 and $162 million in 2018). The revenue of the company was $190 million in 2017. And $1.5 million in 2018 (?!). So I can understand the berserk intensity ratio, but I do not understand the public nature of such a company. They have been spending over the last five years without much to show for revenue. Another open end, yet to be understood.

They have received private placement from many investors. Following snippets from their annual report/ website give an indication of the uncertainty involved in developing new drugs (esp if the company has no other revenue stream):

“Coherus is a leading global biosimilar company. We are committed to improving patient lives by expanding access to life-changing biologic medicines. Founded in 2010 and headquartered in the San Francisco Bay Area, the company is composed of a team of industry veterans with decades of experience in pioneering biologics. Coherus is dedicated to improving patient lives by easing the financial burden of treatment to keep the focus on care, not cost.”

“The Company will need to raise additional funds in the future; however, there can be no assurance that such efforts will be successful or that, in the event that they are successful, the terms and conditions of such financing will be favorable. If the Company is unable to obtain adequate financing when needed, it may have to delay, reduce the scope of or suspend one or more of its clinical trials, research and development programs or commercialization efforts.”

“The Company considers regulatory approval of product candidates to be uncertain, and product manufactured prior to regulatory approval may not be sold unless regulatory approval is obtained. The Company expenses manufacturing costs as incurred to research and development expense for product candidates prior to regulatory approval. If, and when, regulatory approval of a product is obtained, the Company will begin capitalizing manufacturing costs related to the approved product into inventory.”

R&D and Innovation

The companies that spend the most may not be most innovative. The Takeaway #4 is understanding that hgih spend is not equal to high innovation. High efficiency or high RoI spend implies innovation. Following is an extract from the related article by Strategy& where they consider a framework for innovation. They run more analysis with several other metrics of the companies to determine the innovative companies – the companies that use that R&D cost efficiently. (Data for which they have not shared). So I’ll just quote them on the key takeaway on innovation. (which is not measured by R&D spend, but the efficiency of that spend).

“Our analysis reveals that both the high-leverage innovators and the larger universe of companies that report relative high performance have six key characteristics. The first five are widely understood, though executed to varying degrees. The sixth is something that only the best innovators accomplish.

- They closely align innovation strategy with business strategy.

- They create company-wide cultural support for innovation.

- Their top leadership is highly involved with the innovation program.

- They base innovation on direct insights from end-users.

- They rigorously control project selection early in the innovation process.

- They excel at each of these first five characteristics and have been able to integrate them to create unique customer experiences that can transform their market.

For companies looking to improve the reach and results of their R&D investment, examining the strategies of those that consistently perform at the top of their game offers invaluable insight.”

https://www.strategy-business.com/feature/What-the-Top-Innovators-Get-Right?gko=e7cf9

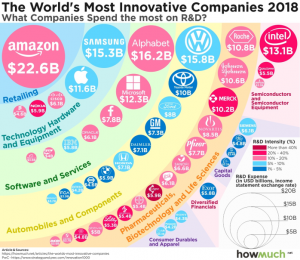

Finally, here are a couple of charts – first one from Howmuch.net which triggered this piece and the second one from Strategy&. Adding here for quick reference. The first chart says “Most Innovative Companies” but as we now understand, most spend does not imply most innovative, so to be considered accordingly. The second chart is more relevant, from the innovation metrics article by Strategy+Business showing their tracking of the most innovative companies over a course of few years.

Note: Following chart is from Howmuch.net

Note: The following chart is from Strategy&

And a final takeaway/note to self. I thought I’ll spend a morning on this. It took me a lot longer. But fun exploration.

Still unanswered questions:

- Are the R&D expenses of certain sectors more capital nature (and hence mainly amortisation is the annual cost) vs recurring annual expenses. I would think the drug development phase in pharma companies which, once successful, will bring in a revenue over a long period of time should be different from something in Tech, where inherent obsolescence of products is higher.

- R&D and tax around the world. Should be easily available, but not keen to explore that path at the moment.

- A look at some of the companies and a look at R&D spend in context of their profitability too. Such as above noted Volkswagen spending almost amount equivalent of OI in R&D. While for Apple, even though the amount is high, still accounts for a relatively much smaller portion of R&D. How would companies justify and argue for such spends?

- Curious about Defense and R&D. Why is the sector not up there?

- Companies like Coherus. A look at more such high spending, early stage companies.

Links referred:

Oil around the world

Capital – some notes (a workbook)