Notes on Lithium

To understand Lithium, its production and dynamics of the market, these notes are drawn and collected from various sources on the internet, linked to the extent possible.

ABOUT LITHIUM

Lithium is a unique element. It is the lightest metal on periodic table. Its ultra-low density (being half as dense as water) combined with its atomic structure gives it an incredibly high electrochemical potential, making it the irreplaceable foundation for modern portable electronics and electric vehicles. This silvery-white alkali metal was first isolated in 1855 by Augustus Mattiessen and Robert Bunsen.

Lithium is a comparatively rare element, does not occur freely in nature, although it is found in many rocks and some brines, but always in very low concentrations. Due to its solubility as an ion, it is present in ocean water. There are a fairly large number of both lithium mineral and brine deposits but only few of them are of actual or potential commercial value.

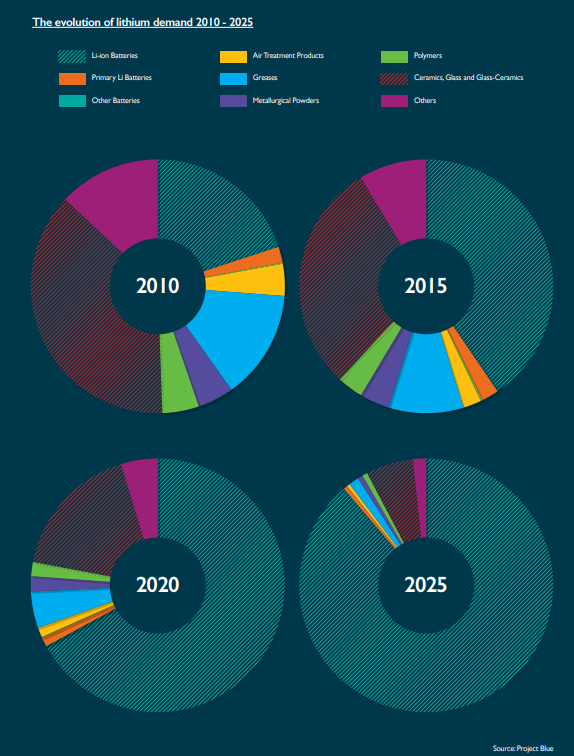

Lithium and its compounds have several industrial applications, including heat-resistant glass and ceramics, lithium grease lubricants, flux additives for iron, steel and aluminium production, lithium metal batteries, and lithium-ion batteries. Batteries alone consume more than three-quarters of lithium production.

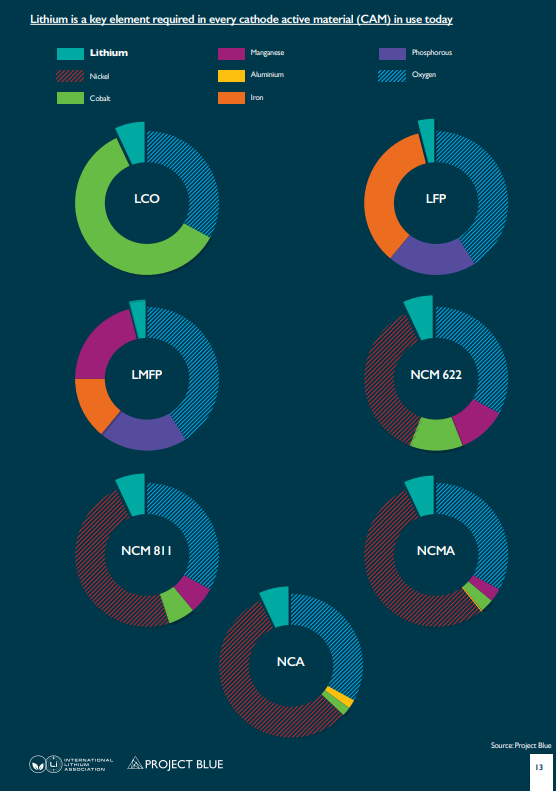

For electric vehicles, lithium is present in all cathode chemistries, representing between 75% and 85% of the cathode raw material cost to date. The physical and electrochemical properties of lithium are what make it an ideal material for use in battery cells. The smaller ionic radius and lighter atomic mass of lithium ions (Li+) compared to other positive ions such as sodium (Na+) or potassium (K+) mean it can achieve a higher capacity-to-weight ratio for battery cells. The smaller ionic radius of the Li+ also allows it to fit into the crystal structure of graphite, allowing less expensive graphite anodes to be used, and combined with its greater diffusion co-efficient also provides greater mobility in the battery electrolyte.

RESERVES AND PRODUCTION

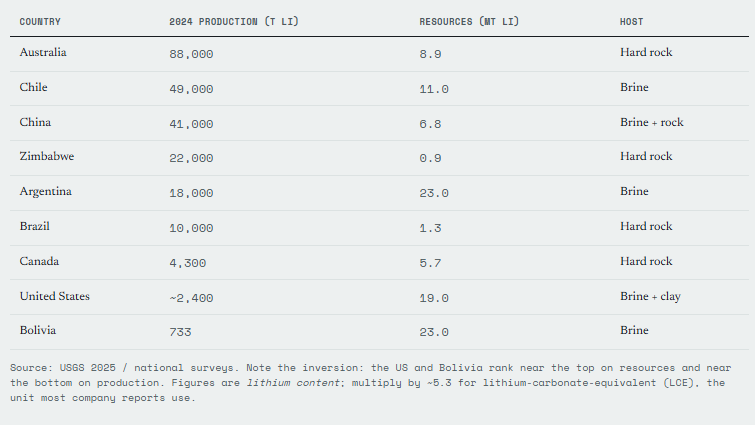

By different counts, the highest reserves are in South America – between Bolivia and Chile. But the largest production of Lithium is done in Australia.

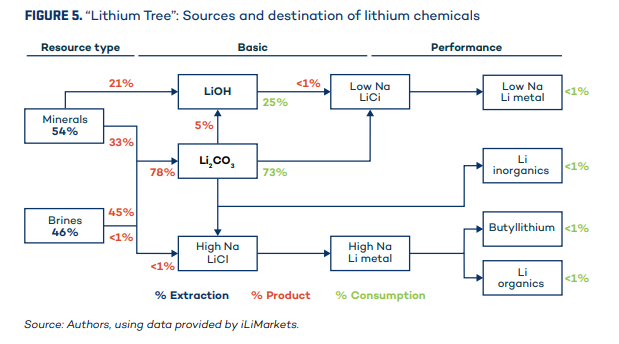

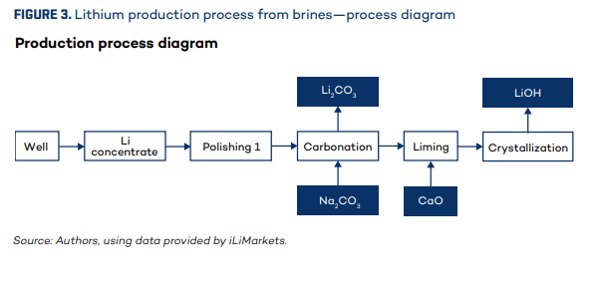

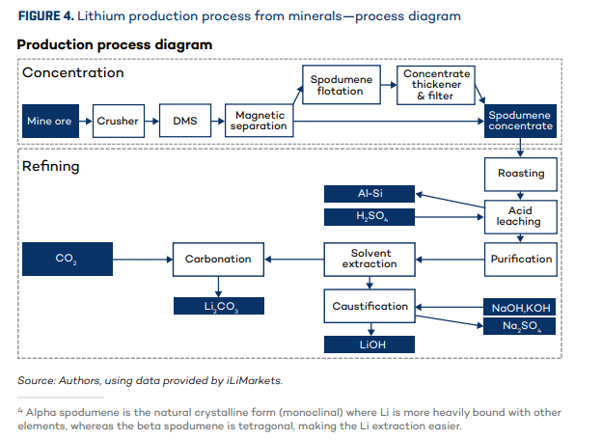

Lithium is traded either in chemical form or as a concentrate. The two dominant chemical forms of lithium on the global market are lithium carbonate and lithium hydroxide. Lithium bearing minerals, such as spodumene, petalite and lepidolite, are mostly sold as concentrates and as direct shipping ore under certain market conditions.

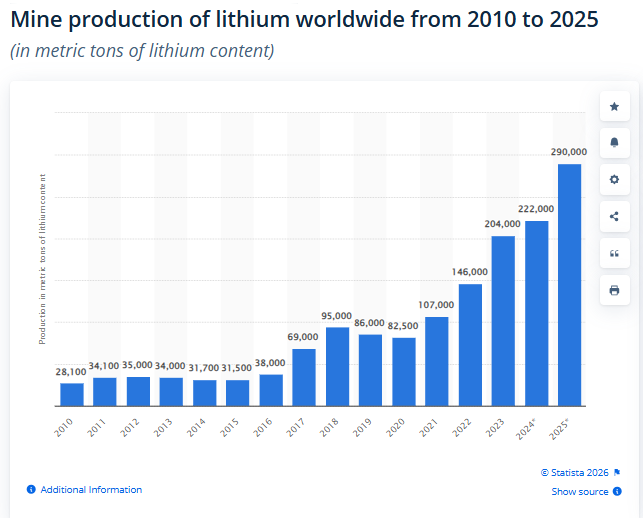

To get a sense of the market, by one source, total Lithium Global Production in 2025 was 290,000 tonnes of Lithium. Of this, 92,000 tonnes was produced by Australia, 62,000 tonnes from Chile and 56,000 tonnes from China. In 2023, production of lithium from brines was dominated by Chile (64%), China (22%), and Argentina (12%). Australia and China were the main producers of lithium from minerals.

This itself is a significant jump from 28,000 tonnes of 2010.

Lithium and its compounds were historically isolated and extracted from hard rock. However, by the 1990s mineral springs, brine pools, and brine deposits had become the dominant source. By early 2021, much of the lithium mined globally came from either “spodumene, the mineral contained in hard rock formations found in places such as Australia and North Carolina” or from salty brine pumped directly out of the ground, as it is in locations in Chile, Argentina, and Arkansas.

Around 77% of raw lithium production still comes from just three countries: Australia, Chile, and China. Australia accounts for roughly 35.2%, Chile for 19.3%, and China for 22.3%.

Regional Production Characteristics:

- South America:Brine-based extraction, low unit costs, climate-dependent production

- Australia: Hard rock spodumene mining, technological leadership, export orientation

- China: Mixed extraction methods, downstream processing dominance, domestic market focus

- Emerging Regions: North America, Africa development projects with strategic government support

Chile, Argentina and Bolivia are also called Lithium Triangle States.

Lithium carbonate equivalent (LCE) standardisation enables direct comparison across diverse production methodologies. One tonne of lithium metal equals approximately 5.32 tonnes of lithium carbonate or 8.56 tonnes of lithium hydroxide, providing the foundation for consistent performance measurement across brine and hard rock operations.

ELECTRIC VEHICLES AND BATTERIES

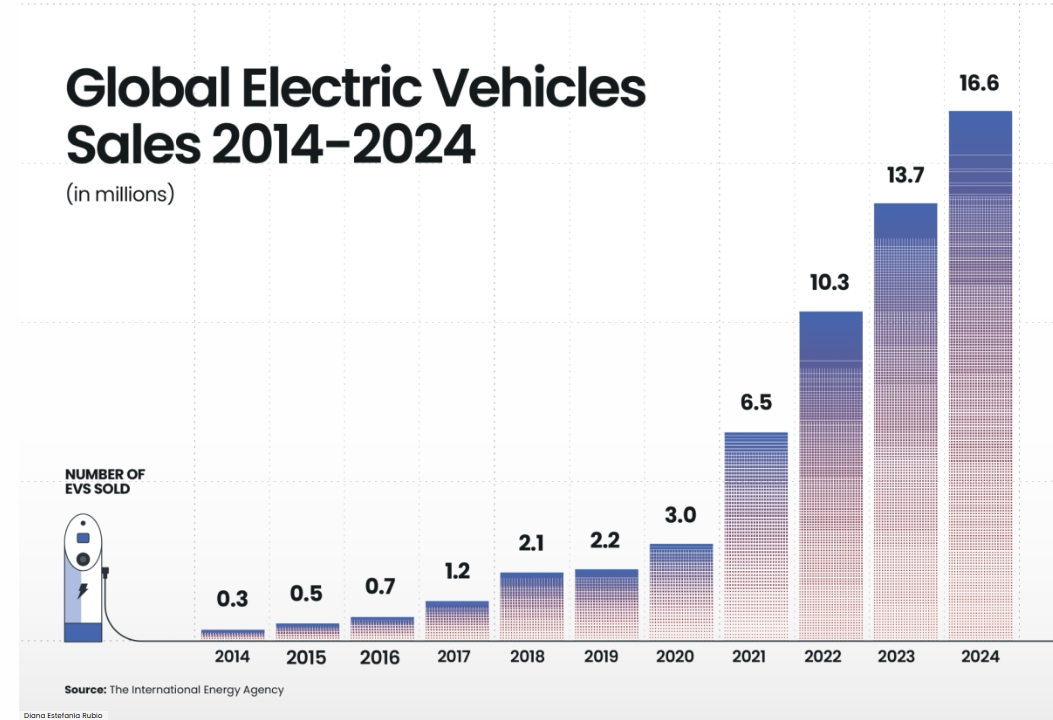

Global electric vehicle sales grew from 6.5 million in 2021 to 10.3 million in 2022 (+60%) and reached 13.7 million in 2023, 16.6 million in 2024. A million electric vehicles consume between 40 and 50 kMT LCE (Lithium Carbonate Equivalent). Almost half of China’s car sales were electric in 2024, representing almost two-thirds of electric cars sold globally.

Electric vehicles could account for 60% of global car sales by 2040. The share of combined BEV and PHEV sales as a function of total vehicle sales is forecast to grow from 20% in 2024 to 35% by 2030 and 60% by 2040.

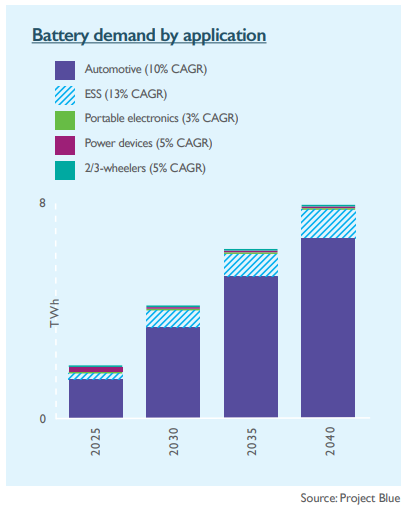

Lithium-ion battery storage is a pivotal enabler of renewables projects by providing flexibility for grid balancing, providing additional electricity during peak times and recharging during periods of low demand.

By 2040, lithium demand is forecast to triple from today’s levels, making it one of the fastest-growing commodities of this, or any, generation. Global demand is expected to grow from 1.3Mt LCE this year to between 3.6Mt and 5.2Mt LCE by 2040.

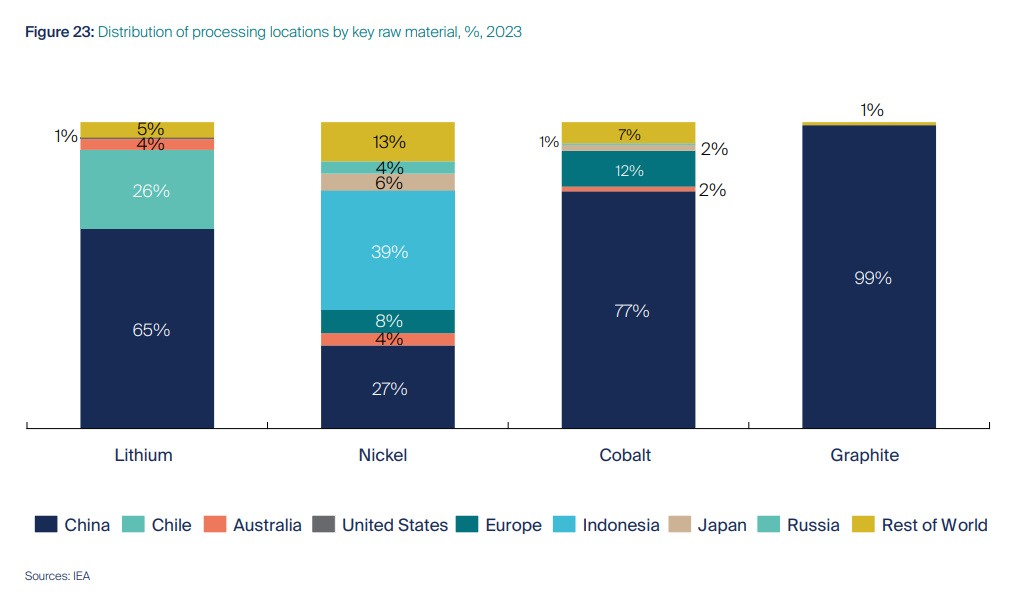

THE SHAPE OF THE INDUSTRY – DOMINANCE OF CHINA

But more importantly, Lithium is not really a “country” industry — it’s a ~10-company industry operating across borders, plus a Chinese refining chokehold. Roughly 65–70% of the world’s lithium refining happens in China regardless of where the rock is dug. Add Argentina and Chile and the top three refining countries reach around 95% of global capacity.

By 2027, Chinese entities are forecast to control around 50% of total global lithium production, up from approximately 35% five years ago. Whoever owns the mine, China largely owns the conversion step.

This concentration risk is not unique to lithium. Across 19 of 20 key transition minerals, China is the largest refiner, with an average share of around 70%. Lithium refining concentration has also increased since 2020 and is expected to remain above 80% through 2035.

Elsewhere, China’s position is built on scale and control across the supply chain rather than on geological abundance or raw ore extraction alone. Its dominance is greatest in refining and processing. The International Energy Agency reports that China refines about 90 percent of REEs (Rare Earth Elements) and is the leading refiner for 19 of 20 key energy-related minerals, with an average global market share of around 70 percent.

The vast majority of global refining of critical battery materials takes place in China, which handles over 65% of the global processing for lithium, cobalt, and graphite.

PRICE AND COST

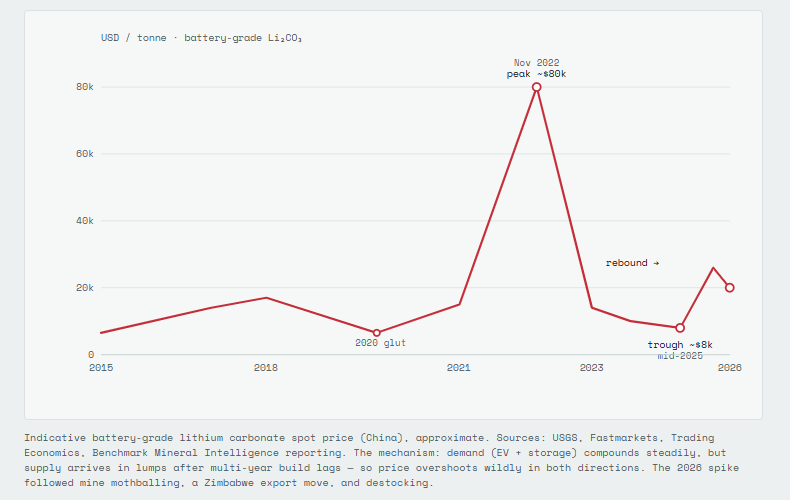

Prices for lithium carbonate in 2024 in the range of $10,000/ton. Upto $20,000 per tonne in 2026.

From another source (explaining the US market prices) :

Lithium carbonate spot prices have been volatile over the past decade, driven by soaring demand and a rapid influx of new lithium projects in response. The oversupply was primarily fueled by the development of spodumene mines in Australia—two in 2017 and five in 2018. By the end of 2019, prices had fallen further to US$7,300 per tonne and by the close of 2020, they had dropped below US$5,000 per tonne. After rebounding sharply in 2021 to US$26,200 per tonne by November, a year later, the prices more than doubled to US$67,000 per tonne, driven by supply constraints and rising demand for EVs.

However, after this historic price surge, lithium prices declined steeply through 2023 and 2024. The decline was largely due to concerns about oversupply, the expiration of Chinese EV subsidies, and EV sales globally being weaker than expected. Lithium supply security has become a priority for technology companies in Asia, Europe and North America. Strategic alliances and joint ventures are being established to ensure a reliable, diversified supply of lithium for battery suppliers and vehicle manufacturers. (From here)

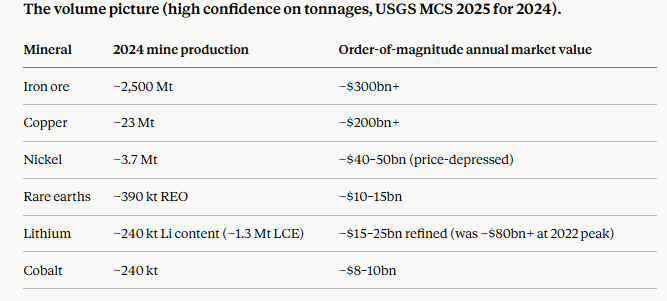

The following table is converted to LCE. According to that calculation Global lithium production reached approximately 1.4 million tonnes of lithium carbonate equivalent (LCE) in 2024, representing a substantial 22% increase from the previous year according to U.S. Geological Survey data.

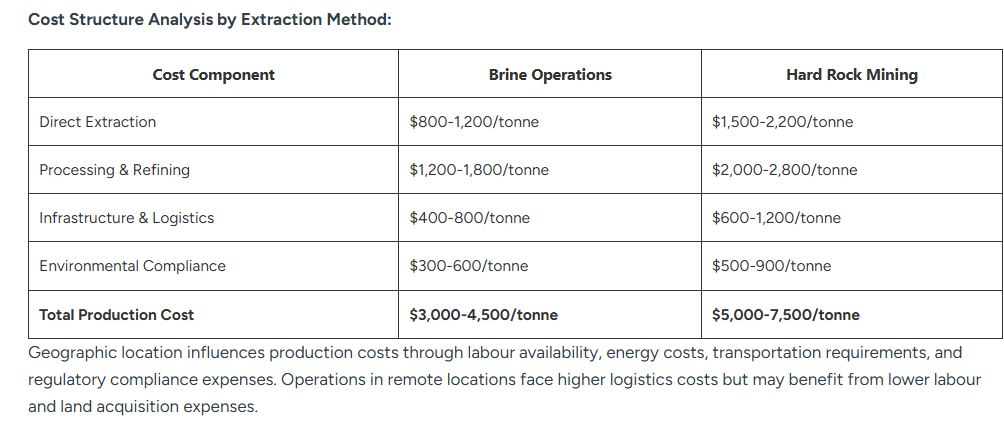

Production cost structures vary dramatically between extraction methodologies, with brine operations demonstrating lower unit costs but higher capital intensity, while hard rock mining requires higher operating costs but offers production timeline advantages.

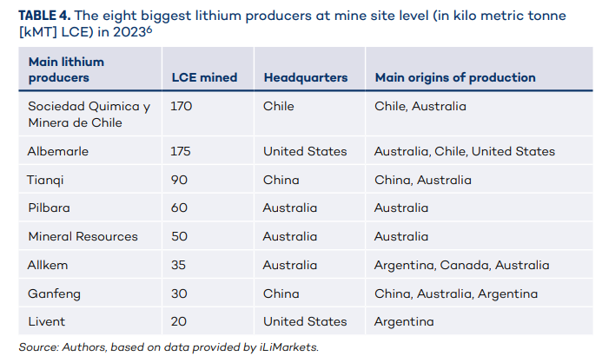

The following are the key producers/companies operating in the Lithium space:

WHY IS IT CRITICAL

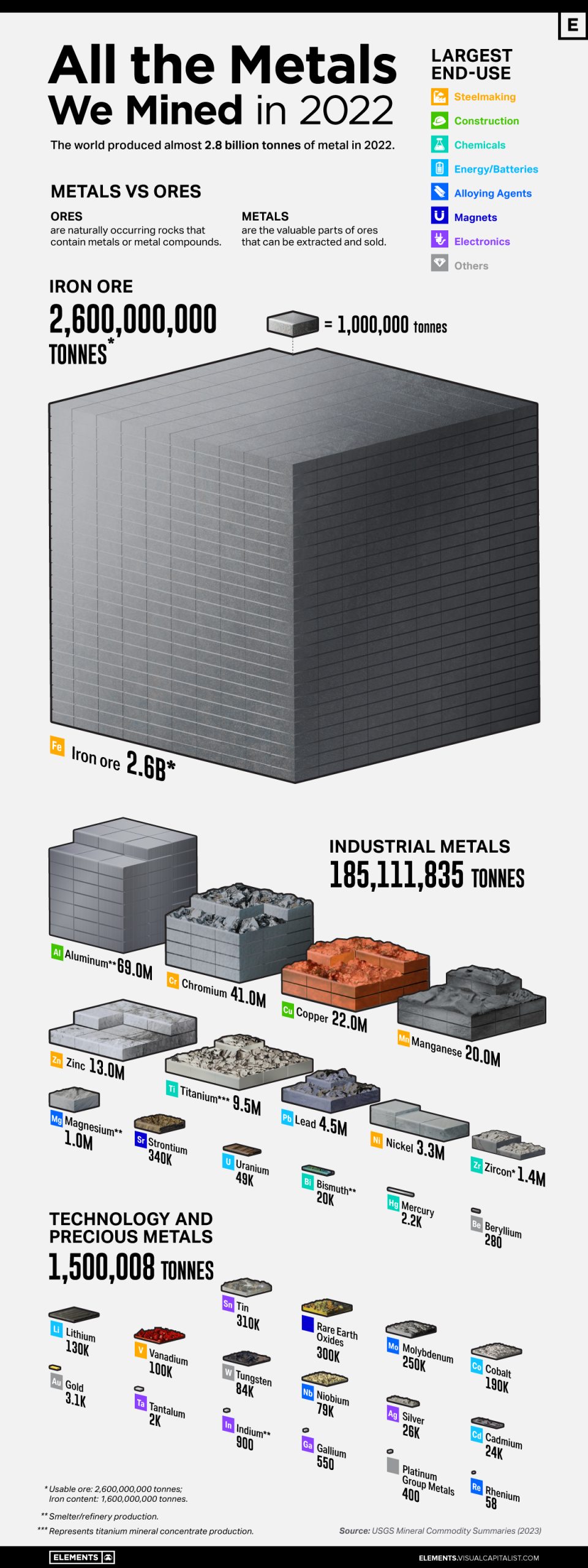

Here’s for context, all the metals mined in the world (dated chart, based on 2021 data, Lithium is more than twice the tonnage now than shown in chart below).

Now, why it’s “critical” despite the size:

- Growth rate. Lithium demand rose by nearly 30% in 2024, against a 10% annual rate in the 2010s, while nickel, cobalt, graphite and rare earths grew 6–8%. Lithium is the fastest-growing of the lot — in the IEA’s net-zero scenario it increases ninefold to 2040.

- No substitute. Batteries account for 87% of lithium use, and there’s no drop-in replacement at current chemistry — unlike, say, nickel-vs-LFP cathode flexibility.

- Concentration. Refining is the choke point — China holds ~70–75% of lithium chemical conversion, and the IEA expects it to supply over 60% of refined lithium in 2035.

*

Further to above, here is an AI-assisted document which explains some of the difference between the two chemistries and their demand profiles. It also adds details on the companies active in the Lithium space.

And for further exploration on Battery minerals and other critical minerals, please see the following links:

Principles of AI usage | Notes towards a framework

Coal – some notes